Chains

BNB Beacon Chain

BNB ecosystem’s staking & governance layer

Staking

Earn rewards by securing the network

Build

Explore

Accelerate

Connect

Careers🔥

Explore Opportunities on BNB Chain

DeFi Outlook 2023

Macro overview

2022 has been an interesting year in crypto, to say the least. The effect of years of expansionary monetary policies has shocked the global economy, significantly lowering DeFi protocol capital and total values locked (TVLs), and forcefully curbing unsustainable growth projections. In 2022 we have witnessed projects, funds and CeFi companies closing shop. Moreover, we have seen how many protocols’ tokenomics, quite lax with emissions, have had a severe impact on their sustainability. The abandonment of these models has put off the table the option of offering disproportionate APYs that are not backed by any type of solid revenue to bootstrap capital. Many DeFi features or products that seemed to work in a bull market, which promised wonders such as capital protection or full hedging also came to nought.

All in all, the past year has been a year of hard learning. Leaving aside some structural and even ethical learnings that have permeated the industry deeply, there have been three major learnings on what is required to hold a strong DeFi ecosystem:

- Liquidity is king: although liquidity is the cornerstone of DeFi, it was largely overlooked by many. The implosion of Luna or the depegging of Lido’s staked ETH (stETH) due to sinking liquidity on its Curve pools showed us how crucial deep liquidity is. Not only bulk liquidity is important, how efficient the deployed capital is utilized (give me a high Liquidity Turnover ratio, LTR!) is even more critical. Protocols that came up with novel approaches to manage liquidity more efficiently (such as Uniswap v3 or iZumi) are gaining more and more market share.

- Real yield: gone are the days of ponzinomics. Long term protocol’s revenue sustainability is necessary. Users love when they get some distribution of the fees or revenues generated by the protocol. We are in crypto for financial inclusion, aren't we? We will see more and more DeFi protocols distributing fees as a way of proving legitimacy and attracting liquidity.

- Innovate, bow your head, build and eventually you will be fine. It might be a long and bumpy road though: a significant portion of the capital deployed in DeFi came attracted by a wide set of factors but stays because of the technology and all the new opportunities that DeFi generates. The protocols that have been laser focused on building, innovating and solving some of the obvious inefficiencies are beginning to reap the benefits today. Who could have told MakerDAO that institutions like Société Générale were going to borrow multimillion-dollar loans in DAI? Projects that innovate tend to hold better in difficult times and experience major growth during the good times.

How has it been for BNB Chain?

BNBChain starts 2023 with quite a rich DeFi ecosystem (more than 500 dApps) with considerable diversification resulting in a strong TVL. 2022 has been a year of deep developments, improvements and filling gaps in the ecosystem. One year ago there was no way to efficiently direct the liquidity of existing stablecoins, the derivatives ecosystem was very small, the relative absence of isolated lending made composability quite complex for many assets and there were no Liquid Staking Derivatives (LSD) either. In just over a year, the BNB ecosystem has matured filling up all these gaps with projects like Wombat and the veWOM aggregators built on top of it (Wombex, Magpie and Quoll), ApolloX and Deri delivering top notch products for derivatives, three different LSD providers competing to offer the best composability of staked BNB and many other projects that are building and bringing hefty value to the chain.

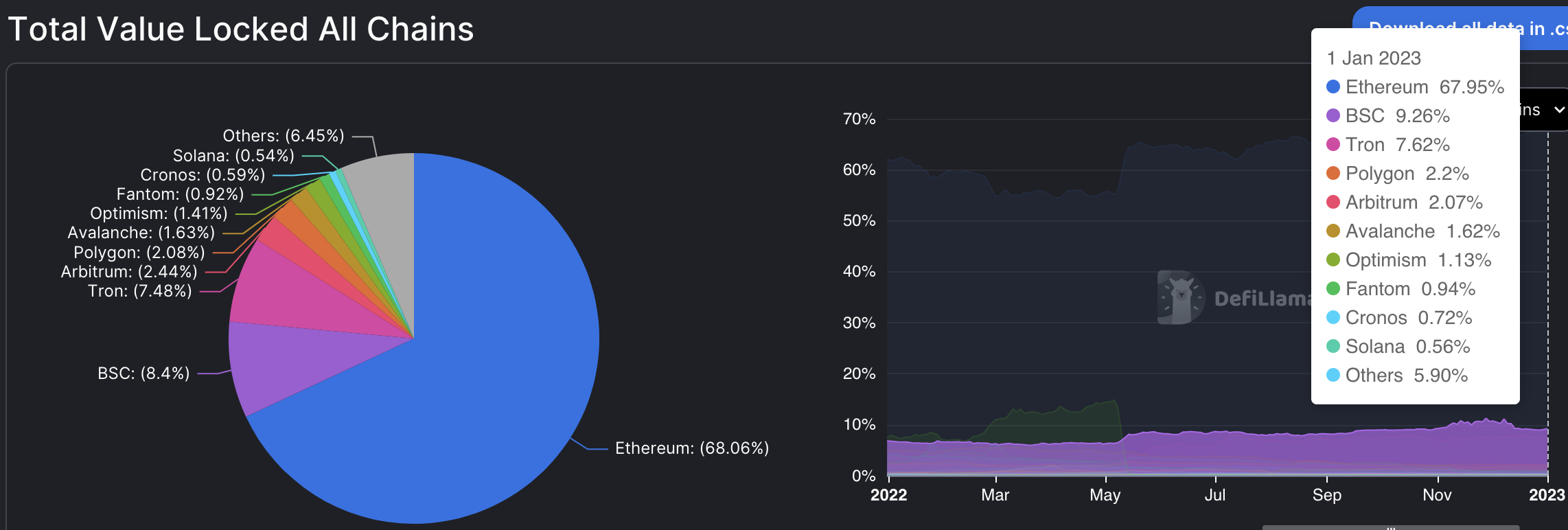

These developments came to fruition. BNBChain started 2022 with a TVL market share of 6% and ended the year around 9% (with a peak of 12%) and significant TVL stability. Also note the significant difference between BNBChain and the alternatives that come right behind in the ranking. The combined TVL of many of them is still smaller than BNBChain alone. Nevertheless, innovation is not the only reason behind these figures. One of the major strengths of BNBChain is its loyal user base, whose metrics (DAU, active wallets...) are also leading across chains, behind much of the adoption BNB DeFi has experienced.

BNB TVL Evolution (Source: DefiLlama)

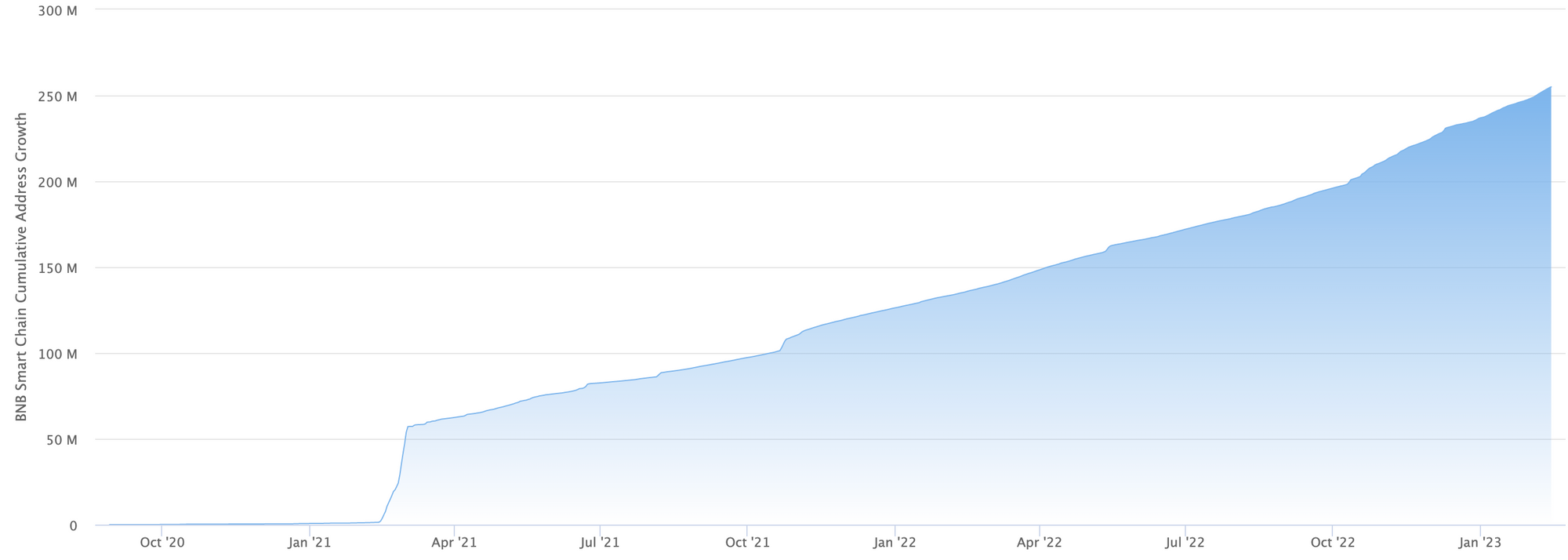

BNB Chain Unique Addresses Chart (Source: BscScan)

Despite all the great improvements and solid market position, there is still a long way ahead to create a flawless DeFi ecosystem and definitely lots of room for growth and innovation. With this piece we want to point out the DeFi categories where we see the most clear opportunities for growth and disruption and invite builders to come join us and build on BNBChain.

Major Developments in DeFi

The biggest developments of DeFi during 2022 can be clustered into two large groups. Optimization of inefficiencies and narratives (trends) that emerged to fill up existing gaps in DeFi.

- DeFi is a young industry that was unveiled to the world during the DeFi summer of 2020 (you can chuckle, we all miss those days). Like any nascent industry backed by a technology that is still in its teens, inefficiencies are kind of widespread. This hampers financial development as capital is still highly inefficient in comparison with traditional finance. Problems such as impermanent loss, liquidity inefficiency and low LTR of Automated Market Makers (AMMs), hyper collateralization or the difficulty of isolating risks in common pools are some of the problems that are yet an issue. These entail a big problem for the DeFi base layer, liquidity (AMMs) and lending. These inefficiencies limit the correct development of more complex layers built on top of them and especially hinder mass adoption.

Protocols such as Uniswap with concentrated liquidity (Uniswap v3) or Euler with isolated pools, avoidance of collateral rehypothecation or MEV-resistance liquidations try to put an end to these structural deficiencies. New lending versions like Venus v4 also go down that path, adding some of these improvements to its products. Others have emerged purely to solve inefficiencies in existing protocols, such as Arrakis to facilitate the allocation of liquidity by LPs on Uniswap v3 or Morpho, to limit the spread between borrow and Lend APYs due to low capital utilization in lending markets.

- The narratives come to fill gaps in the DeFi ecosystem. Narratives normally include a set of projects that, although building in the same direction, hold significant differences. It is around these narratives where great innovation and developments are generated and therefore, are very important growth vectors. DeFi's increasing synergies between different protocols mean that more and more types of projects can now enter a given narrative.

Some of the narratives that we believe may generate major developments during this year becoming crucial for the DeFi are Derivatives (from perps to options), Synthetics, Liquid Staking Derivatives and a come-back of the Blackhole narrative (remember the Curve wars?). Due to the, mainly legal, peculiarities (licenses, KYC required...) of RWAs, it is likely that we will see a slower development that might not generate such a solid momentum. But even so, we expect significant growth around protocols bringing on-chain off-chain assets or going in the opposite direction, making on-chain capital available to non crypto firms.

It is at the intersection of both groups where we think most of the innovation and DeFi developments will happen during 2023. Nevertheless, these are certainly not the only areas with great growth expectations. We develop further in the lines below.

Which DeFi areas will generate the most growth and adoption?

Let’s start with the basics, there is still a lot to improve in swapping and lending...

It is easy to forget the basics and the most foundational DeFi primitives. AMMs with their liquidity pools and lending markets are the engine that drives DeFi. Indeed, most of the capital deployed in DeFi is allocated to liquidity or lending pools. Even so, significant disruption is still possible and much needed in these areas.

On the side of the AMMs, the main factor to optimize is liquidity management. We will probably see that projects that directly address improvements in capital utilization with concentrated or even asymmetric liquidity models will manage to bootstrap more and more liquidity and absorb a significant number of txs from obsolete liquidity approaches. Also, there is a growing need for projects that can make liquidity provision more profitable for liquidity providers. Most of them still lose money.

Trading Volume Evolution Uniswap V2 vs V3 (Source: Dune @David_C )

One of the main use cases of any asset in DeFi continues to be lending or borrowing. Despite large capital allocations to lending markets, we believe that the market opportunity for new players in this area is still very large. This will be especially the case for projects that tackle MEV liquidation frontrunning, oracle manipulation, permissionless listing, high degree of capital utilization or mitigation of bad debt. Protocols like Euler or Morpho have proven the appetite of the market for lending projects that solve inefficiencies still present on most of the market leaders.

Liquid staking, one of the major DeFi developments. A crucial underlying monetary layer in the making

Staking is a great product, probably one of the most organic yield sources on crypto while also helping secure the network. Despite this great combination, high capital requirements of most chains and tech requirements prevent most of the market participants from accessing its wonders. Rocket Pool and Lido came up with the intelligent idea of delegating user’s tokens to protocols that have the sufficient firepower to participate in staking and distributing the staking rewards to these users. For that they created a derivative, known as Liquid Staking Derivatives (LSDs). LSDs can be used on other DeFi dApps as for example collateral, letting their holders to leverage on their tokens (from lending to providing it as liquidity). A new way of using an interest bearing token, fully powered by DeFi mechanics, as a liquidity base layer.

The demand around LSDs is so high that Lido has become the first DeFi protocol by TVL across chains. Many centralized players like Binance, Coinbase and Kraken offer their centralized counterparts. Protocols like Frax are coming with innovative ways of boosting staking rewards with its sfrxETH and frxETH duality. BNB liquid staking has been one of the DeFi categories that grew the most in 2022 and generated significant traction. A small ecosystem is also flourishing around LSDs. One of the most interesting use cases for liquid staked BNB is found on Helio protocol, where it can be used as collateral to mint the destablecoin HAY. Redacted Cartel will follow suit on Ethereum with its LSD backed stablecoin Dinero.

frxETH and sfrxETH Mechanics

Coming back to ETH LSDs, we expect a growing demand around it as we get close to the Shanghai upgrade. This traction will not be isolated to the Ethereum network. As interoperability between chains grows, top crypto assets will become more and more relevant on the chains they are not native to due to their powerful tokenomics and liquidity. The staking rewards of LSDs makes them one of the most profitable options to get exposure to ETH on the BNB Ecosystem. Therefore, it is likely that more and more protocols will be looking into LSDs to build new functionalities and products. bETH, frxETH and sfraxETH are already live on BNBChain and we anticipate that more use cases would be formed around them. We also expect that more projects and developers will notice how strong BNB as an asset is and the possibilities that building a solid LSD ecosystem around it could bring and come to the chain to compete with the existing LSD providers or to deliver new use cases for liquid staked BNB.

This might be the year when finally synthetics take off

Synthetics are a long acquaintance for many. Minting an asset that can give you exposure to any single asset as long as there is some oracle price feed to bring it on-chain sounds great. A real bridge between DeF and TradFi. Despite these great prospects, synthetics have still not truly taken off. With oracle tech improving by leaps and bounds, more regulated players bringing trust and the growing needs of DeFi to get exposure to assets that are kept on balance sheets instead of registered on the blockchain.

Synthetics' roadmap of GMX

Synthetics open the door for many new use cases. From CDPs (Collateral Debt Position) using commodities as collateral, to 24/7 markets or by being used as decentralized derivatives liquidity layer. Synthetics are set to play a major role in DeFi and we hope to see an important footprint of these assets in the upcoming top DeFi projects. They are already in the spotlight of many top developers and 2023 will be an important year for synthetics’ development.

Blackholes: Remember the Curve Wars? They could be back

Curve and its veCRV token model changed the way the DeFi industry understood liquidity and emissions for good. Teams like Convex or Frax rapidly figured out how crucial veCRV ownership could become for their projects (to for example maintain deep liquidity of FRAX pools) and started accumulating as many vested tokens as possible. They went one step ahead and built new vested layers on top of veCRV, incentivizing users to lock their tokens for long periods of time. Bribes and other features started popping up to maximize veToken holders’ fees. Although to many this was just an unnecessary over-layering approach, markets are not always efficient and might need external help to get closer to the concept that got Eugene Fama an economics prize that bears the name of a famous Swedish explosives inventor. A clever liquidity management makes capital become more efficient and less dispersed. This might be detrimental for many protocols with low resources but makes most of the liquidity deep enough to hold large trades and volumes. For the proper function of any DeFI ecosystem, liquidity should be quite big in the most traded pools, instead of being scattered throughout the ecosystem. The Curve Wars have put something very relevant in perspective, liquidity has a price and the protocols must be willing to pay for it.

We expect to see great innovation and profound changes in the blackhole market as its importance becomes more and more latent. Frax has shown that veTokenomics is a long term play, but also the enormous benefits it can have for a protocol. FRAX was the only non-fully collateralized (fractional) coin that did not plummet during the Luna collapse. Although the difference in architecture also played a role in this, a big reason was the deep liquidity that Frax protocol had redirected to its liquidity pools by controlling lots of veCRV. Frax protocol has been able to benefit from these dynamics on its LSD offering. Frax created a a dichotomy between sfrxETH which accrues staking rewards and frxETH which does not. sfrxETH offers the highest staked ETh APY. Even so, many liquidity providers are more attracted by frxETH because Frax pools are heavily boosted by Frax protocol.

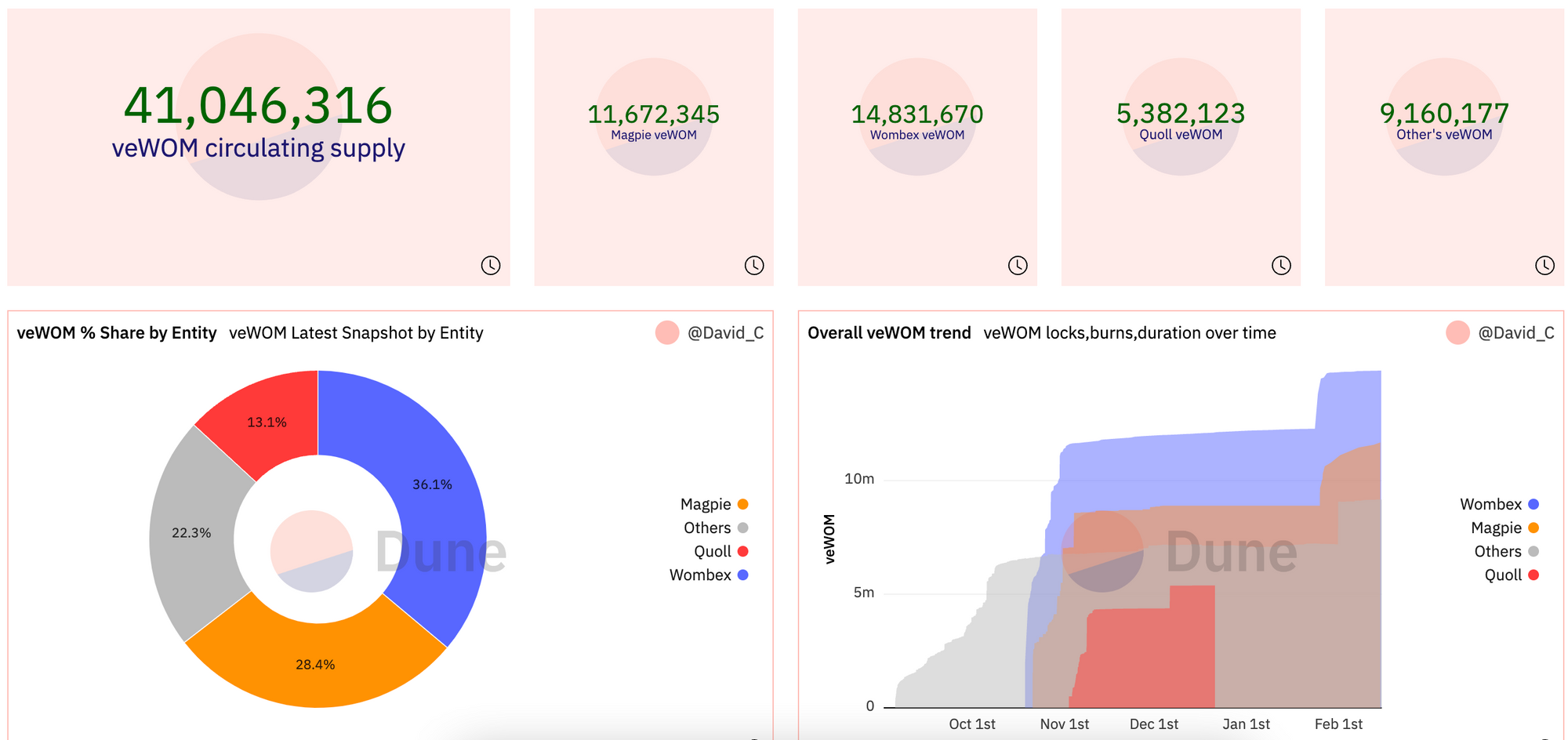

During the last quarter, BNBChain's appetite for veModels has been displayed with the reception that Wombat and the different veWOM aggregators have received from the community. We expect more projects to build in this area in 2023 attracted by this demand.

WOM Wars (Source: Dune @David_C )

Is 2023 gonna finally be the year of Decentralized Derivatives?

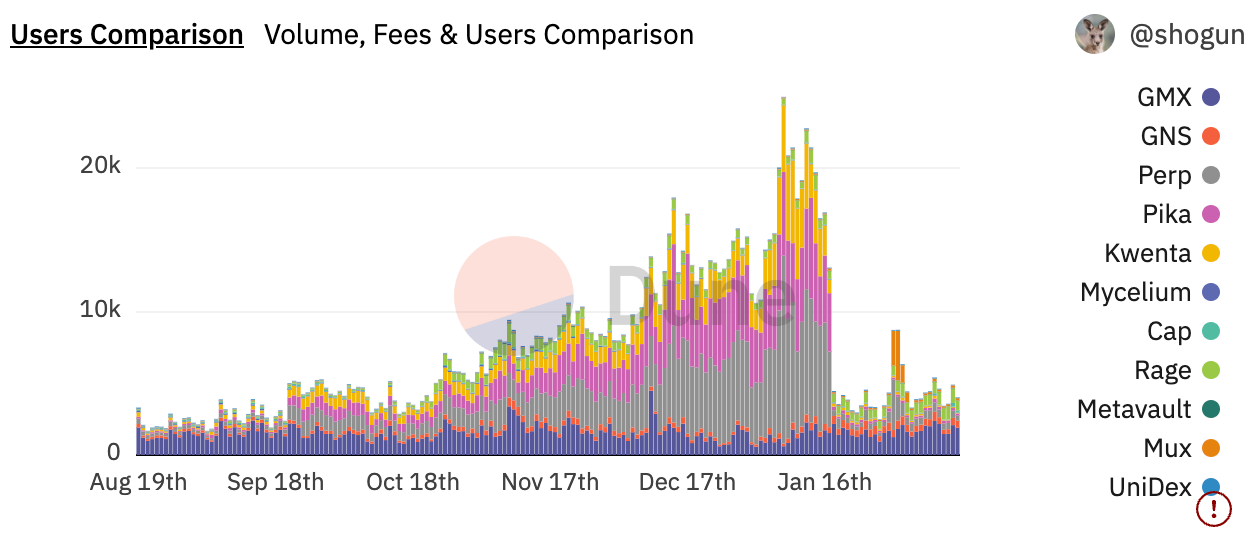

Already in 2022 the decentralized derivatives narrative began to take off. GMX with its GLP pool generated a paradigm shift, moving the classic operation from off-chain orderbook to fully on-chain. This model allows new layers to be built on top of what is now known as a DDEX (Decentralized Derivatives Exchange), from structured products to social trading. The volumes of decentralized perpetuals do not stop growing, ApolloX had a volume over $2B in January. ApolloX has recently launched its on-chain ALP pool, making the protocol a hybrid version between pool model and order-book. These new architectures let new protocols use the perps or liquidity of these pools as a basis for launching new products and features, so we expect many projects to start building here. With each passing month it becomes clearer that the demand for decentralized perpetuals is becoming more important.

Users evolution of major Perpetuals Protocols - missing ApolloX and Deri (Source: Dune @shogun)

Options has been the dormant giant of DeFi for years. As the market matures, new financially savvy users will be using DeFi more and more. Options are an essential financial instrument for any investor, so we expect their demand to increase making decentralized options a great area to create projects around. Option vaults are a good option for those users who either do not want to incur the hassle of thinking in options Greeks or just want to buy a certain strategy. We also expect that those protocols that can simplify the use of options, as well as the UX (it is still difficult to understand what the strike price is with the naked eye in many projects), will grow exponentially. Using binary options or options as underlying for prediction markets marketed in a simple way, we believe will attract a significant chunk of on-chain activity. Freedom of architecture around options (similar to OTC derivatives in TradFi) will also be crucial for the growth of this category. Projects like Vyper Protocol seem to have understood this and are building amazing on-chain options products with the customization level of institutional-grade products.

As the development of synthetics grows, it is to be expected that derivative protocols will increasingly start using performance against synthetics as underlying more and more. The growth possibilities that this offers are much greater as the exposure to assets grows exponentially, becoming a very attractive product to build and use.

Real-World assets and tokenization, the ultimate financial bridge

Bringing the vast amount of off-chain assets on chain while letting players outside of DeFi to benefit from the wonders of it (quicker processes, increased access to capital, increased capital efficiency for example by freeing up working capital) is about what Real World Assets (RWAs) are about. During the last two years we saw how more and more companies were using RWAs to access on-chain capital through players like Centrifuge, while granting exposure to on-chain lenders to off-chain assets or cash flows. Tokenization of financial vehicles is slowly growing thanks to protocols like BackedFi. Nonetheless, the offer of RWAs protocols is still very limited. We believe that it is a matter of time before this changes, especially in a macroeconomic environment in which the cost of capital is growing every day, expecting significant growth on protocols building in this domain.

Additionally, we expect to see a proportional growth of protocols that allow on-chain access to financial assets considered RWA through tokenization that are fully backed by the underlying. These protocols will make financial vehicles such as ETFs fully transferable on-chain, generating new opportunities to leverage and build over these assets which will be fully collateralized and held by some custodian. Compliance and a clearer regulatory landscape might be crucial for these products, therefore, licensed players will hold a competitive advantage in this domain. We expect that in the coming years RWAs will be one of the largest DeFi adoption vectors as well as a relevant source of on-chain capital.

DeFi is coming to NFTs

2021 was a year full of developments (and also hype) around NFTs. Most of the traction came in the form of communities popping up around them, partnership and lots of technical developments. Nevertheless, beyond NFTs for gaming, there were not many cases around these new assets. NFTs became JPEGs, hyped internet pictures or cool digital sneakers. During the year 2022, developers set their sights on these assets to provide them with new use cases, lending was one of the most developed ones. We believe that we will see an expansion and solid adoption of these types of protocols over the next few years. Already in January we have seen certain NFTfi projects reach all-time highs in borrowable capital. This might be just the beginning.

Wrapping up

We have tried to summarize the biggest growth drivers for DeFi last year and the ones that we think will drive 2023/2024 growth. We will see a big focus on deep and optimized liquidity, revenue sharing fleeing from ridiculously inflationary ponzinomics, increasing composability and interconnectivity (on the same chain and across chains) topped with a simple UX in the leading protocols.

BNBChain is bringing more and more top talent to build on the ecosystem while also attracting more and more native projects from other chains. On early February two leading blue-chips – Uniswap and Euler – decided to come build with us. On the other hand, BNBChain flagship native projects such as Pancakeswap are as well becoming crucial on other ecosystems (first DEX on Aptos). BNBChain has established itself as one of the most relevant DeFi ecosystems in an industry that is definitely going multichain and this is being noticed by many.

This piece’s ultimate goal is a call to builders who are building in any of these categories, regardless of the degree of development of their protocols to deploy on BNBChain. This is also a call for VCs that are looking to help their portfolio projects to find a good place to land or where to expand. Connect with us and help us push the ecosystem forward, the largest and most loyal user community is waiting for you.

Also, let's speak on Twitter !

Programs for builders

BNB Chain runs together with Binance Labs the Most Valuable Builder accelerator. It's 6th edition is still opened to applicants and for DeFi we are specially looking for projects building LSD solutions, derivatives and structured products, lending and ZkKYC. We also have the BNB Chain Builder Grants for projects contributing to the ecosystem, you can apply here. Finally, our 6-month virtual Bootcamp-hackathon-Incubator program zero2hero is focused on developers that want to grow their very own dApp in the BNB Chain ecosystem.

Disclaimer

Digital asset prices can be volatile. The value of your investment can go down or up and you may not get back the amount invested. No communication or information provided to you is intended as, or shall be considered or construed as, investment advice, financial advice, trading advice, or any other sort of advice. Any project or protocol referred to in this article should not be construed as a recommendation, vetting, or endorsement of such third-party projects by BNB Chain, or any other affiliated entity. We do not and cannot control activity that community participants may develop using BNB Chain, which is a public, decentralized and permissionless blockchain. We disclaim any responsibility or liability for any interactions or engagement you may have with these protocols and projects. You should always perform your own due diligence, including consulting your own independent professional or specialist advisors, to determine if a particular opportunity is suitable for you.